In this, the 150th year since British Marine’s foundation, we aim to publish a series of short articles throughout the year highlighting the key moments in the birth and development of the marine insurance industry from the beginnings of the first hull clubs to the emergence of mutual protection and indemnity associations.

British Marine’s heritage is deeply intertwined with the unique story of these clubs, their shipowner members and the innovative insurance solutions that emerged over time. It is a story that we are proud of and, despite challenges and changes over the centuries, one which informs our culture and way of doing business today, even as we continue to navigate risk into the future.

Genesis: From Hull to Protection & Indemnity

In 1720, Royal Charters for dealing in marine insurance were granted only to Royal Exchange Assurance, London Assurance and Lloyd’s of London. In practice, rates for the insurance of ships were typically set by a small body of subscribers at Lloyd’s, whose rates were widely followed in regional insurance markets throughout the United Kingdom. By the early 1800s regional shipowners in places such as Bristol, Glasgow and Newcastle became disillusioned with what they perceived as a costly, distant market with often unreliable underwriters and brokers. Even in the best cases, many insurers were bankrupted by heavy ship losses during times of war, leaving shipowners unpaid.

The emergence of mutual social organisations for individuals and families – the ‘Friendly Societies’ – in the UK in this period captured the attention of shipowners, who alongside their peers began to seek collective solutions to their perceived difficulties in obtaining reliable insurance for their ships. Shipowners beyond London were the first to move towards a form of self-help characterised by mutualisation, with the colliers of Newcastle and the north-east of England traditionally credited with the creation of the first mutual hull clubs. By 1800 there were around twenty such clubs offering mutual insurance for hulls.

This simple shift in where insurance could be obtained was not without its difficulties though, as many of these early hull clubs operated with minimal working capital. Premiums for entry were effectively a flat deposit and, with little in the way of what we would today recognise as skilled underwriting, it was only through strict control of their memberships that owners of better run ships avoided being beholden to the misfortunes of the poorer ones. Local knowledge of the shipowner, their ships and their trades were a subjective but necessary qualification of entry to a hull club, leading to the establishment of clubs based on region, trade, or ship type.

Questions over the legal legitimacy of these early clubs were tested in Parliament, eventually leading in 1824 to the withdrawal of the monopoly protection under the Charters of 1720. By the mid-1800s, the difficulties arising from the hull clubs’ mix of ‘good’ and ‘bad’ members had created appetite for new specialist marine insurance companies with tighter control of entry and underwriting practices. Six new companies were launched in 1859 alone, with another six founded between 1860 and 1964, many of which survive in some form today.

These new clubs were considered operationally superior and more reliably solvent, leading owners of better-quality tonnage to move their ships from the older hull clubs with flat entry premiums to the newer ones where they could obtain cheaper insurance on the back of their better claims performance due to more sophisticated underwriting. As a result of declining ship quality, increased claims and difficulties in collecting supplementary premium payments from an increasingly disparate membership, many of the old hull clubs closed in the mid-1800s. This left in place the mutual clubs that we recognise today.

Legislative changes in the UK in the latter half of the 1800s exposed shipowners to an increasing array of liabilities for which they would turn to their mutual clubs for a solution. The early hull clubs were established to insure the hull and equipment (machinery, as we know it today) only, and had not previously envisioned risks beyond physical damage to a shipowner’s property. Owners began to seek ‘protection’ from the new liabilities they were facing under the law, and the mutual clubs responded to their members’ needs by expanding the types of insurance covers they would underwrite.

In 1836 the collision between LA VALEUR and FORBES in India gave rise to a dispute that, after arbitration, saw each owner having to bear half the cost of the substantial repairs. LA VALEUR’s underwriters refused to pay the difference between the repair costs and the total amount paid out to the owner of FORBES because they deemed this element not to be a ‘peril of the sea’. Standard hull policies typically excluded one‑quarter of collision damage and limited recovery to the insured value of the vessel, regardless of the damage caused to others. As ships became larger and more valuable, these restrictions increasingly exposed owners to uninsured losses. In 1854 clubs incorporated the 3/4ths Running Down Clause (RDC) provision in P&I policies. This limited underwriter’s liability to 75% of the cost of any claim arising from a collision.

From this point onward, the mutual clubs began to cover a greater number of additional risks shared by their common members, such as wreck removal, quarantine and cargo damage expenses. These additions to mutual cover generally followed the broadening liabilities shipowners were facing because of legislative developments. The Fatal Accidents Act 1846, for example, made employers responsible for acts of negligence that caused the death of a seafarer in their employ. Two cargo claims in 1870, on the WESTHOPE and the EMILY, saw shipowners lose claims to cargo owners for deviation from a contracted destination and for faulty navigation.

Liability exposure increased further with the Merchant Shipping Act 1854, which consolidated earlier maritime legislation and formalised shipowners’ responsibilities for safety, discipline, wrecks and casualties. The Act strengthened regulatory oversight by the Board of Trade and clarified legal procedures relating to maritime incidents, significantly increasing the likelihood of claims arising from accidents at sea.

Shipowners turned once again to mutual solutions. Drawing on the model of the earlier hull clubs, they established Protection Clubs to cover liabilities arising from injury and loss of life, and Indemnity Clubs to address collision liabilities exceeding hull policy limits. By the late 1800s these functions were increasingly combined, marking the birth of Protection and Indemnity insurance.

The formation of British Marine

British Marine Mutual Insurance Association Ltd. was incorporated in London by Edward Reid Evans under the Companies Act on 29th February 1876. Evans had been a manager of seven mutual clubs, all of which were brought under the umbrella of the new mutual. One of the seven of the clubs was the Iron Club, established specifically to cover ships made of the revolutionary new material. Another was the United Kingdom Trawler’s Mutual (UKTM), covering a sizeable fleet of fishing vessels as remains the case today. The club moved with the times, insuring at first sailing ships and, increasingly, the new iron hulls that began to dominate British shipbuilding and merchant shipping from the 1850s onwards. British Marine insured the world’s first all welded ship, Anchor-Brocklebank Line’s FULLAGAR.

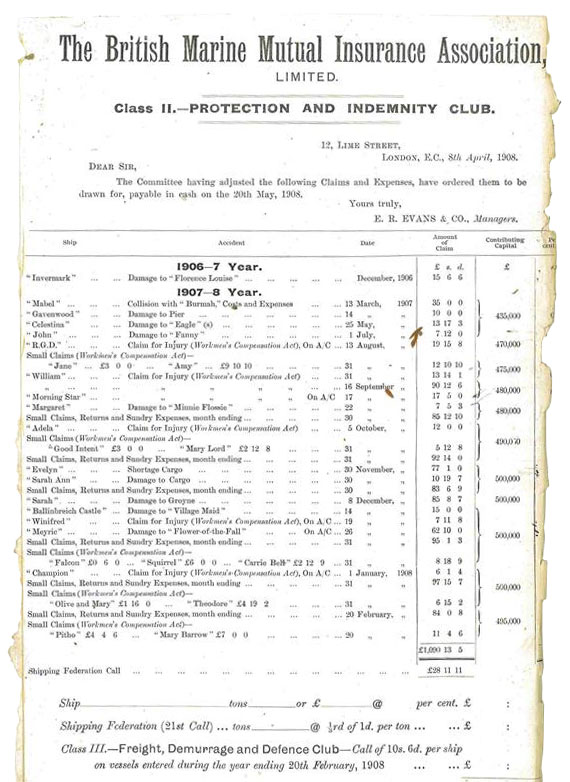

Seven classes of insurance existed for different categories of ship and trade, with their new existence under one mutual effectively allowing shipowners to choose where to trade, even on a world-wide basis. Rules were fully specified and linked to the Articles of the Association, further standardising the cover provided. A separate agreement was made for the management of British Marine by E.R. Evans & Co. Over the years various classes of cover were developed, being either retained, amalgamated or even dropped as the cover reflected continued technological developments in shipping. In 1894 the class for wooden hulled ships was closed and British Marine rationalised into four main classes: Hull, P&I, Defence, and Collision. British Marine had evolved so significantly that a little over 40 years from its birth as a hull club, in 1908/09, claims for crew injuries under the Workmen’s Compensation Act (1897) accounted for 50% of the value and 70% of the number of P&I claims paid.

Social attitudes and marine technology had clearly changed, but British Marine existed for the very purpose of reflecting the ever-changing needs of its membership. In this sense, something akin to the modern P&I clubs and insurers of today can confidently be said to have existed by the turn of the century. Four distinct classes of cover provided specific risk insurance services for unspecified types of ships, the rules became general, and the rating of individual ship entries was becoming more detailed and sophisticated. It was the outbreak of World War One in 1914 that led to the creation of a fifth class of business that survives to this day; War Risks.

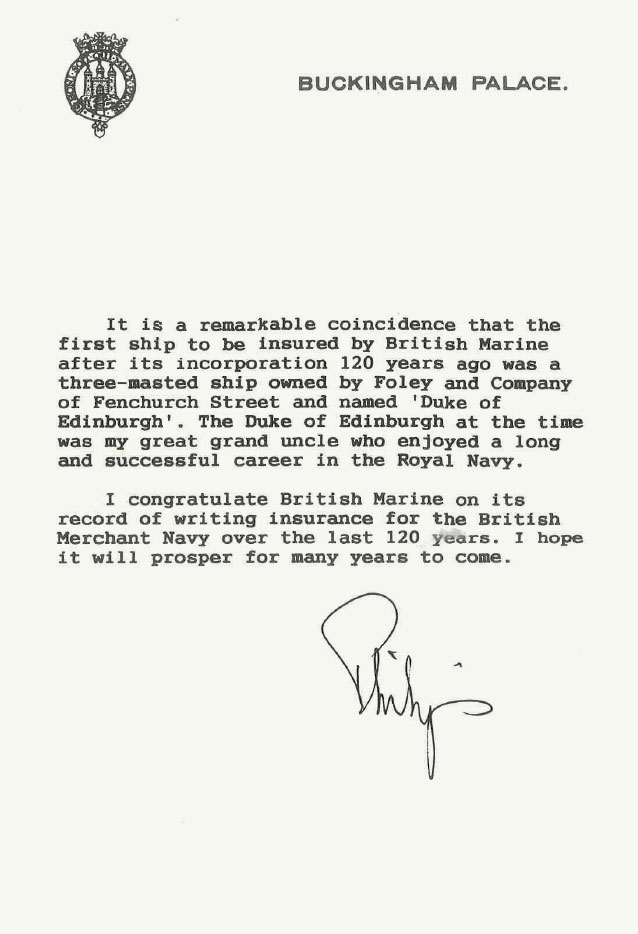

A forward from the late His Royal Highness The Prince Philip, Duke of Edinburgh